View this article online: https://www.insurancejournal.com/news/southeast/2023/08/07/734164.htm

Stakeholders near and far are hailing a near-record number of takeouts from Citizens’ Property Insurance Corp. as a sign that the troubled Florida insurance market is improving, even if it will likely mean higher premiums for homeowners.

“This is what happens when you have real insurance reform,” Louisiana insurance defense attorney Matthew Monson wrote on his Linkedin page last week.

He argued that after Florida lawmakers in the last two years approved major reform measures that limited one-way attorney fees and assignment-of-benefits agreements, insurance companies are now showing a willingness to invest in the state, and he urged Louisiana lawmakers to adopt “Florida style” reform.

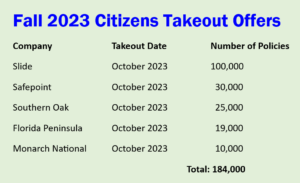

Monson was speaking specifically about Tampa-based Slide Insurance Co., which the Florida Office of Insurance Regulation approved to offer takeouts to as many as 100,000 Citizens policyholders – far more than any other carrier. Safepoint Insurance was approved for another 30,000; followed by Southern Oak, with 25,000; Florida Peninsula, with 19,000; and Monarch National with 10,000.

Altogether, that’s 184,000 policies that could be removed from Citizens, the state-created insurer of last resort that has ballooned to become Florida’s largest property insurer, with more than 1.3 million policies in force this year.

“I think, as far as the insurance market in Florida is concerned, I think that this is an encouraging sign,” Citizens spokesman Michael Peltier told WFLA TV news.

Citizens officials have tried to tamp down the insurer’s rapid growth in recent years, launching a depopulation program, raising rates slightly, and ordering more inspections of properties. Last month, the Citizens Board of Governors also approved spending $36 million on a new clearinghouse software platform, designed to make it easier for agents to find private carriers with comparable premiums.

But with a statutory glidepath that limits rate increases to no more than 12% annually, property owners have flocked to Citizens – simply because its premiums are the lowest in many parts of the state. The huge assumption by Slide suggests that the primary market is starting to catch up and at least some insurers are now willing to expand their exposure in windswept Florida.

Citizens policyholders by law cannot stay with Citizens if a takeout offer’s premium is within 20%. So some insureds may have to leave the state-backed insurer but may not end up with the assuming company. The Slide offer would assume the policies Oct. 17, the OIR consent order notes. The takeout follows a May order that granted Slide some 25,000 Citizens policies.

The consent order did not indicate the dollar amount of premium that Slide will inherit on the assumed policies. Although Florida law allows Citizens to pay a bonus to insurers as an incentive to assume Citizens policies, as much as $100 per policy, the July 31 consent order notes that no incentives will be paid in this case.

“Slide understands that the selected policies to be assumed … will not be subject to any incentive or bonus plan, whether statutory or otherwise,” the consent order reads. Peltier said that the bonuses have not been offered for a “very long time.”

Slide’s CEO, Bruce Lucas, told the Artemis news site that if most of the 100,000 policies do go to his firm, it would be a major increase in size for the carrier, which now has about 175,000 policies in force.

Lucas and the OIR ruffled some feathers in the Florida insurance market in 2022, when the fledgling Slide was allowed to take on some 147,000 policies and $90 million in unearned premiums from insolvent St. Johns Insurance Co., while other insurers were left out of the deal. Early this year, Slide assumed 91,000 policies from United Property & Casualty Insurance while it was in a runoff but shortly before it, too, went insolvent.

At the time, executives at a few other insurers argued that OIR should have moved the St. Johns and UPC policies to Citizens, then let carriers make takeout offers. Granting policies and premiums to Slide left the Florida Insurance Guaranty Association holding millions of dollars in claims, forcing FIGA to sell bonds and levy assessments on all Florida insurers, some said.

Lucas told Insurance Journal that those concerns are misplaced.

“If Slide had not stepped in to assume policies from companies that had become insolvent, those companies would have incurred even more deficiencies that FIGA would also have to cover,” he said in an email in July.

Susanne Murphy, the former Florida deputy insurance commissioner for property and casualty who stepped down late last year, said that in general, when a private carrier can seamlessly take over thousands of policies it makes life much easier for policyholders, particularly in a hard market like Florida’s.

“As a general rule of thumb, the goal of the receiver and OIR is to provide the insurance consumer with continuation of coverage,” Murphy said recently.

Six months after the UPC insolvency, Slide, founded in 2021, could be on the cusp of a 60% increase in size, thanks to its own takeout offer for Citizens policies. It’s another sign the market is rebounding, along with improved bottom lines for the second quarter of 2023 for other Florida carriers, some have said.

“I remain bullish on the Florida homeowners market moving forward,” Lucas said last month. “Recent legislative reforms addressed several key issues including removing one-way attorney fees, shortening the statute of limitations, and getting rid of assignment of benefits. Florida homeowners need better insurance options, and Slide is accelerating our expansion in Florida to meet these demands.”

OIR has approved other big takeout plans in past years, and Lucas has participated. In fall 2012, the office granted approval for 210,000 offers, with some 90,000 policies going to American Integrity Insurance and 75,000 to Homeowners Choice Property & Casualty.

Another 60,000 went to Heritage Property & Casualty, which had just been founded by Lucas that year.